It’s one of those unspoken rules of the Indian middle class. One should know the difference b/w Life insurance vs mutual funds before starting an investment. We love things that “give something back.” We hate the idea of paying for something and getting nothing in return if we stay alive. Agents know this. They play on this “Paisa Vasool” mentality. But the reality is, by trying to get your premium back, you might be losing out on lakhs, or even crores, over a lifetime.

I’ve spent years looking at portfolios where people are “insurance rich” but “wealth poor.” They have ten different policies, but none of them actually provide enough cover to protect their family, nor enough returns to fund their retirement. It’s a classic Khichdi (mess) that benefits the seller more than the buyer.

YOU CAN ALSO READ:

SIP vs lumpsum investment during market highsThe Story of the “Guaranteed” Trap

Take my friend Vikram. About fifteen years ago, a family friend convinced him to start a “Wealth Creator” plan. It was an endowment policy. Vikram was told he’d pay ₹50,000 every year for 20 years, and at the end, he’d get a “guaranteed” lump sum plus some bonuses. It sounded safe. It sounded like a “double benefit” life cover plus savings.

Ten years in, Vikram showed me the policy. We did the math. The life cover was only ₹5 lakhs. (For context, Vikram’s annual expenses were already ₹8 lakhs). If something happened to him, that ₹5 lakhs wouldn’t even cover his family for a year.

And the returns? After factoring in the bonuses, the projected IRR (Internal Rate of Return) was hovering around 5.5%. At that same time, inflation in India was averaging 6-7%. Basically, Vikram was losing purchasing power every single year while thinking he was “investing.”

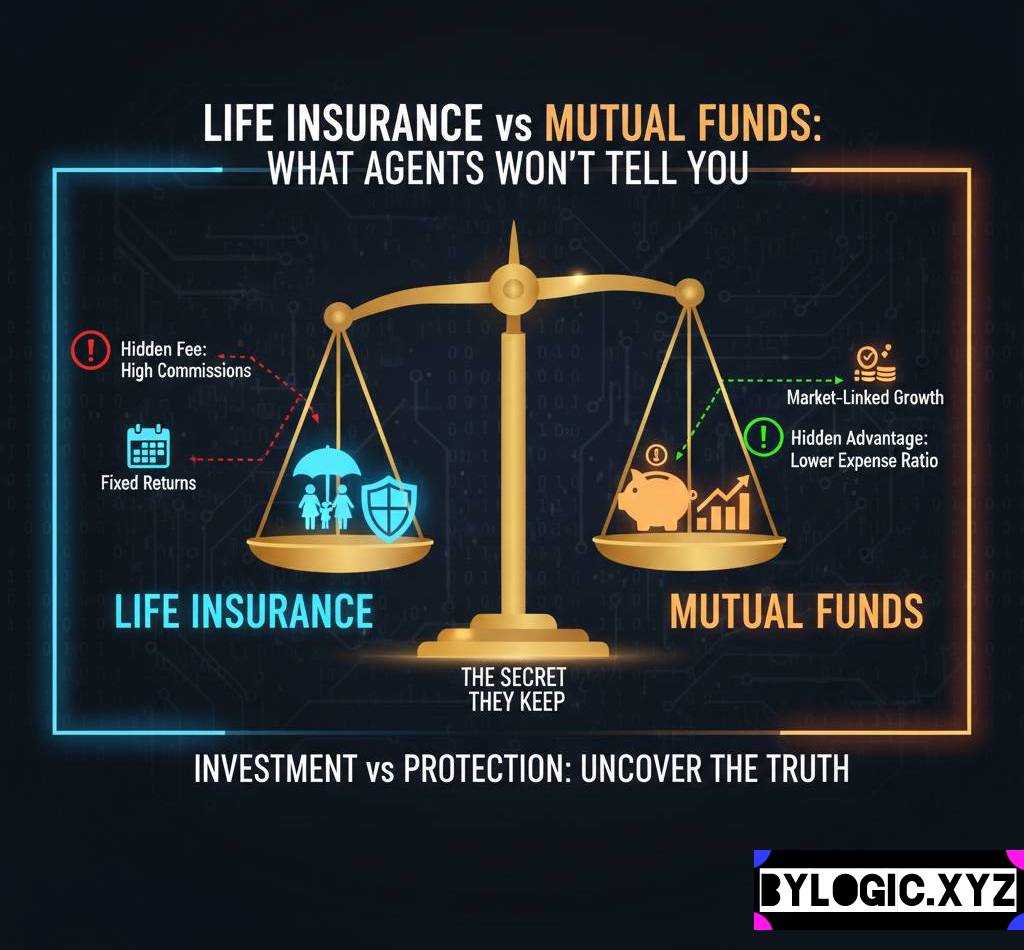

The Lesson: Insurance is for protection. Mutual Funds are for wealth. When you try to marry the two, you get a spouse who doesn’t cook and doesn’t work.

The Dirty Details: What the Brochure Hides

Agents often use fancy charts to show you “Projected Benefits.” What they rarely mention is the Cost of Management. In a Mutual Fund, the expense ratio is transparent usually between 0.5% to 2.25%. In many traditional insurance plans, the “allocation charges” and “agent commissions” in the first few years can be as high as 30-35% of your premium.

Think about that. If you give ₹1,00,000, only ₹65,000 is actually working for you in the first year. The rest is gone to the agent and the company’s office rent. In a Mutual Fund SIP, almost the entire ₹1,00,000 starts compounding from day one.

Let’s look at how they stack up side-by-side.

Comparison: The Reality Check

| Feature | Life Insurance (Endowment/ULIP) | Mutual Funds (Equity/Hybrid) |

| Primary Goal | Mixed (Protection + Saving) | Wealth Creation |

| Transparency | Low (Hidden charges/bonuses) | High (Daily NAV, Expense Ratio) |

| Liquidity | Poor (Lock-ins, Surrender charges) | High (Can withdraw anytime*) |

| Expected Returns | 4% to 7% (Usually) | 10% to 15% (Market linked) |

| Flexibility | Rigid (Must pay premium to keep it) | High (Can stop/skip SIPs) |

Commentary: See that liquidity part? That’s the real killer. Life happens. You might need money for an emergency, a house renovation, or a better opportunity. With a Mutual Fund, you can sell your units and get the money in two days. With a traditional insurance policy, if you try to get your money back in the first 3-5 years, the “surrender value” is often zero or a fraction of what you paid. It’s a trap that forces you to keep paying for a bad product just to “save” what you already put in.

Opinion: In my view, ULIPs (Unit Linked Insurance Plans) have improved lately with lower costs, but they still don’t beat the flexibility of a separate Term Plan + Mutual Fund combo. Why give an insurance company control over your investment strategy?

YOU CAN ALSO READ:

How BNPL (Buy Now Pay Later) traps middle-class usersWhy Agents Won’t Tell You About Term Insurance

If you ask an agent for a Term Plan (pure insurance with no return), they might say, “But beta, you’ll get zero at the end if you survive! Why waste money?”

Here’s why they say that: The commission on a ₹15,000 Term Plan is peanuts. The commission on a ₹1,00,000 Endowment Plan is a vacation to Thailand.

But if you buy that ₹15,000 Term Plan, you get a ₹1 Crore cover. If you take the remaining ₹85,000 and put it into a Nifty 50 Index Fund or a decent Flexi-cap Mutual Fund, the math changes completely. Over 20 years, that ₹85,000 annual investment at 12% could grow to nearly ₹68 lakhs. Your endowment plan would probably struggle to hit ₹30-35 lakhs.

Wait, let me repeat that: By separating the two, you get 20 times more life cover and double the wealth.It’s a no-brainer. But of course, your agent’s car isn’t going to fuel itself on your Term Plan premium.

How to: Decouple Your Finances

If you’ve already realized you’re stuck in a bad “investment-cum-insurance” plan, don’t panic. You don’t always have to stop it immediately, but you should definitely stop adding more.

- Calculate the Surrender Value: Call the company or check the portal. If you’ve only paid for 2 years, you might lose the money. If you’ve paid for 5+, you might get some back.

- Buy a Pure Term Plan First: NEVER cancel your old policy until your new Term Plan is active. You need that safety net.

- Start a Simple SIP: Don’t overthink it. A simple Index Fund is a great place to start.

- Make the Old Policy “Paid-Up”: If the surrender charges are too high, ask if you can make the policy “paid-up.” This means you stop paying premiums, the life cover reduces, but you don’t lose the money you’ve already invested; you just get it back at maturity.

Common Misconceptions (The “Lafdas”)

- “But I get tax benefits under 80C!” Both Insurance and ELSS (Equity Linked Saving Scheme) Mutual Funds give you tax benefits under 80C. Don’t buy a bad product just to save 30% tax. You are still losing the other 70% to a slow-growing asset.

- “Mutual Funds are risky, Insurance is safe.”Risk is relative. The biggest risk is not having enough money for your child’s education 15 years from now because your “safe” investment didn’t beat inflation. Mutual funds have market volatility (ups and downs), but over the long term (7+ years), they have historically outperformed almost everything else.

- “My agent will help me with claims.”Claims are settled by the company based on your medical history and documentation, not the agent’s “influence.” As long as you are honest in your form, your family will get the claim.

The Final Word: Life insurance vs mutual funds

At the end of the day, financial planning isn’t about finding the “best” product; it’s about finding the right tool for the job. You wouldn’t use a screwdriver to hammer a nail, even if the screwdriver was “guaranteed” to last 20 years.

Insurance is for the “what if” of death. Mutual funds are for the “what if” of life.

Keep them in separate boxes. Your family will have a much bigger safety net, and your bank balance will actually reflect your hard work rather than your agent’s commission. It might feel “boring” to pay for a Term Plan and get nothing back, but the “return” you get is the freedom to invest aggressively elsewhere.

Stop being the agent’s favorite client. Start being your family’s best CFO.

YOU CAN ALSO READ:

Term insurance myths that cost families lakhsDisclaimer: Please consult your financial advisor before taking any financial decision regarding surrendering policies or starting new investments.

Explore more categories:

https://bylogic.xyz/category/investing-and-wealth-building/

https://bylogic.xyz/category/loans-and-credit/