Have you met with people in life, who talks the most about their “big wins” in the stock market is often the same one who can’t tell you their actual total return over the last five years? It’s a classic case of noise vs. signal. Even small mistakes that destroy long-term returns can quietly compound over time.

When you first start investing, it feels like you’re entering a high-stakes game where everyone else has a secret manual. You see the green and red candles, you hear terms like “breakout” or “short squeeze,” and you feel this frantic urge to do something. But here is the irony: in the world of long-term wealth, the more you “do,” the less you usually make.

YOU CAN ALSO READ:

Personal loan rejection reasons banks never explainI’ve seen brilliant people doctors, engineers, even accountants completely trash their retirement portfolios not because they were “unlucky,” but because they kept tripping over the same basic hurdles. These aren’t just “errors”; they are return-killers that eat your compounding for breakfast.

The “Get Even” Trap: A Story of Emotional Anchoring

Let me tell you about a friend of mine, Rohit. Back in 2021, when everything was going to the moon, Rohit bought a “hot” tech stock at ₹500. He was convinced it was the next big thing. Three months later, the stock dropped to ₹350.

Instead of looking at the company’s failing fundamentals, Rohit said, “I’ll sell it once it gets back to ₹500. I just want my money back.”

He waited. The stock went to ₹200. He waited more. It went to ₹120. Rohit spent three years holding a dying business because his ego wouldn’t let him accept a ₹150 loss. Meanwhile, if he had sold at ₹350 and moved that money into a simple Index Fund, he would have recovered his losses and been in profit by now.

The Lesson: The market doesn’t know what price you bought at, and it doesn’t care. Holding onto a loser just to “break even” is like staying in a bad relationship just because you spent a lot on the first date. It’s a waste of time and capital.

The Comparison: Investing vs. “Gambling in Disguise”

Most beginners think they are investing, but they are actually participating in a high-adrenaline hobby. Let’s look at the differences in how they play out over time.

| The “Gambler” Mindset | The “Investor” Mindset |

| Check prices: 10 times a day. | Check prices: Once a quarter. |

| Strategy: Buying what’s trending on social media. | Strategy: Buying based on a pre-set asset allocation. |

| Reaction to crash: Panic-selling to “save” what’s left. | Reaction to crash: Buying more (if the plan allows). |

| Fees: Pays 2% in high-churn brokerage & taxes. | Fees: Stays low-cost with passive funds or long holds. |

| 10-Year Result: Usually underperforms inflation. | 10-Year Result: Significant wealth creation. |

Commentary:

The “Gambler” gets the dopamine hit, but the “Investor” gets the beach house. The biggest mistake is thinking that activity equals results. In most parts of life, the harder you work, the better you do. In investing, the less you fiddle with your portfolio, the better it grows.

Opinion: I’ve realized that the best thing a beginner can do is delete their trading app from the home screen. If you have to go through three steps to check your balance, you’re less likely to make a “snap decision” because some guy on the news looked worried.

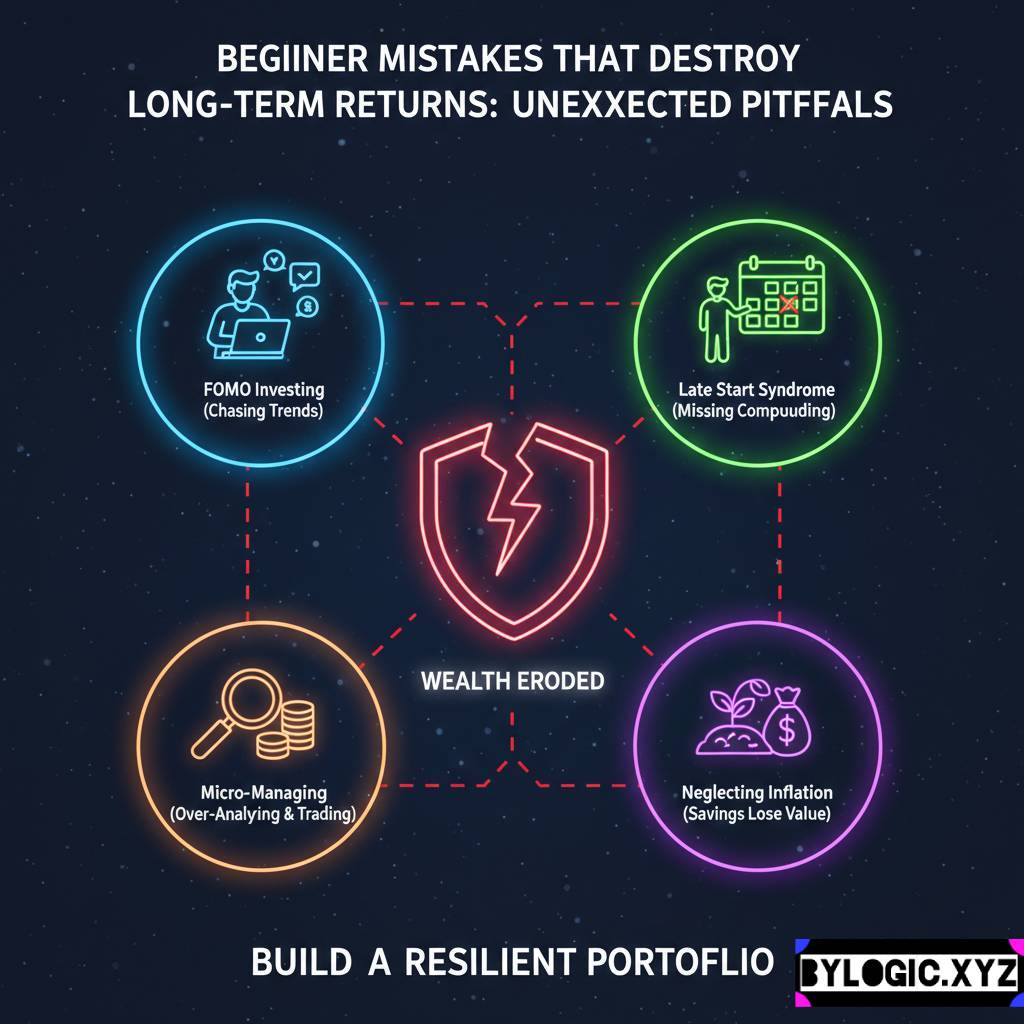

The Silent Killers: 3 Mistakes That Trash Your Returns

1. Chasing “Hot” Tips (The FOMO Fever)

If you are buying a stock because your brother-in-law or a YouTube influencer said it’s “guaranteed to double,” you aren’t investing; you are being the “exit liquidity” for people who bought months ago. By the time a tip reaches the general public, the smart money is already leaving.

YOU CAN ALSO READ:

Home loan vs rent: complete cost comparison for 20 years2. The “SIP Stopper” Syndrome

When the market falls 10%, beginners often stop their Systematic Investment Plans (SIPs). They say, “I’ll wait for things to settle down.”

This is the equivalent of a store having a 50% off sale and you saying, “I’ll wait until the prices go back up before I buy anything.” You want the market to be down when you are buying! That’s when your money buys more units.

3. Ignoring the “Boring” Math (Fees and Taxes)

A 1% extra fee doesn’t look like much today. But over 20 years, it can eat up nearly 25-30% of your total final wealth. Many beginners buy “Regular” mutual funds instead of “Direct” ones, or they trade so often that they lose a massive chunk to Short Term Capital Gains (STCG) tax.

How to: Set Your Portfolio on “Auto-Pilot”

If you want to avoid these traps, you need a system that protects you from yourself. Here is a simple “How to” for building a sturdy foundation:

- Step 1: The “Life Jacket” (Emergency Fund): Never invest money that you might need for your rent or medical bills in the next 12 months. If the market dips and you are forced to sell to pay a bill, you’ve already lost.

- Step 2: The “Rule of 3”: Stick to three simple things an Index Fund (for growth), a Debt Fund/PF (for stability), and maybe some Gold (for insurance). You don’t need a portfolio of 25 different stocks.

- Step 3: Automate Everything: Set up your SIPs to go out on the day your salary hits your account. If the money never sits in your bank account, you won’t spend it on a new iPhone, and you won’t “forget” to invest when the market looks scary.

- Step 4: The 24-Hour Rule: Never buy or sell based on a news headline immediately. Give yourself 24 hours to sleep on it. Usually, by the next morning, the “urgency” disappears.

The “Guru” Misconception: Mistakes that destroy long-term returns

We often think that successful investing requires being a “math whiz.” It doesn’t. It requires being an “emotional whiz.”

I’ve seen people with PhDs in finance lose everything because they thought they could outsmart the market. Meanwhile, my neighborhood auntie, who has been putting ₹5,000 into a boring large-cap fund for 15 years without ever checking the “NAV,” is sitting on a small fortune. She didn’t have a better strategy; she had a better temperament.

Reality Check: The market is basically a mechanism for transferring money from the “impatient” to the “patient.” If you check your portfolio daily, you are exposing yourself to 50/50 odds of seeing red or green. If you check it once every 10 years, the odds of seeing green are nearly 100%.

Final Thoughts

Look, mistakes are part of the journey. You will buy a bad stock at some point. You will feel the sting of a market crash. The goal isn’t to be perfect; it’s to avoid the “catastrophic” mistakes that reset your progress to zero.

Stop looking for the “Next Big Thing.” The current “Big Thing” is compounding, and it only works if you stay out of its way. Don’t be the person who restarts their 20-year journey every 2 years because they got bored or scared.

Build a boring plan, automate it, and go live your life. The best thing your money can do for you is grow quietly in the background while you focus on things that actually matter.

YOU CAN ALSO READ:

Budgeting Made Simple: The 50-30-20 Rule with real exampleDisclaimer: Investments in the securities market are subject to market risks. Past performance does not guarantee future results, and all information provided is for educational purposes. Ask your financial advisor before making any moves, especially when the market feels like a roller coaster.

Explore more categories:

https://bylogic.xyz/category/digital-payments-banking-and-personal-finance-tools/

https://bylogic.xyz/category/insurance-life-and-health/