Most people don’t even know the idea of Asset allocation by age and treat investing like a grocery list. They hear about a “hot” small-cap fund from a colleague, buy some gold because their parents said so, and keep a chunk in a savings account because, well, paisa safe rehna chahiye (money should stay safe). But if you look at their portfolio, it’s usually a chaotic mix of random decisions made at different points in time. There’s no “why” behind the “what.”

I remember talking to a friend, Rahul, who is 28. He was brag-showing me his portfolio last year. It was 95% equity mostly mid and small caps. He was riding the bull market high. Then the market took a 5% breather, and he was panicking, asking if he should sell everything. That’s the problem. He had the “age” for high risk, but not the “stomach” for it, and definitely no “buffer” in debt or gold to keep his head cool.

YOU CAN ALSO READ:

Index funds vs active funds: 10-year return realityAsset allocation isn’t some complex math reserved for fund managers. It’s basically just deciding how to split your money so you don’t have a heart attack when the markets dip, but you also don’t end up with returns that can’t even beat inflation.

The “Rules” vs. Reality

You’ve probably heard the classic “100 minus age” rule. If you’re 30, you put 70% in equity (100 – 30) and the rest in debt. It’s a decent starting point, but honestly? It’s a bit too simple for the messy lives we lead. It doesn’t account for your kids’ school fees, your aging parents’ health, or that sudden urge to quit your job and start a cafe.

Here is how the three big players Equity, Debt, and Gold actually behave in your life:

- Equity (The Growth Engine): This is your Ferrari. It goes fast, but it’s bumpy. You need this to build wealth over 10-20 years.

- Debt (The Shock Absorber): This is the suspension. It won’t make you rich, but it stops you from hitting your head when the road gets rough. It’s your FDs, PPF, and Debt funds.

- Gold (The Insurance): Gold is that weird friend who shows up when everyone else is failing. When the economy looks scary, gold shines. It’s a hedge, not a primary growth tool.

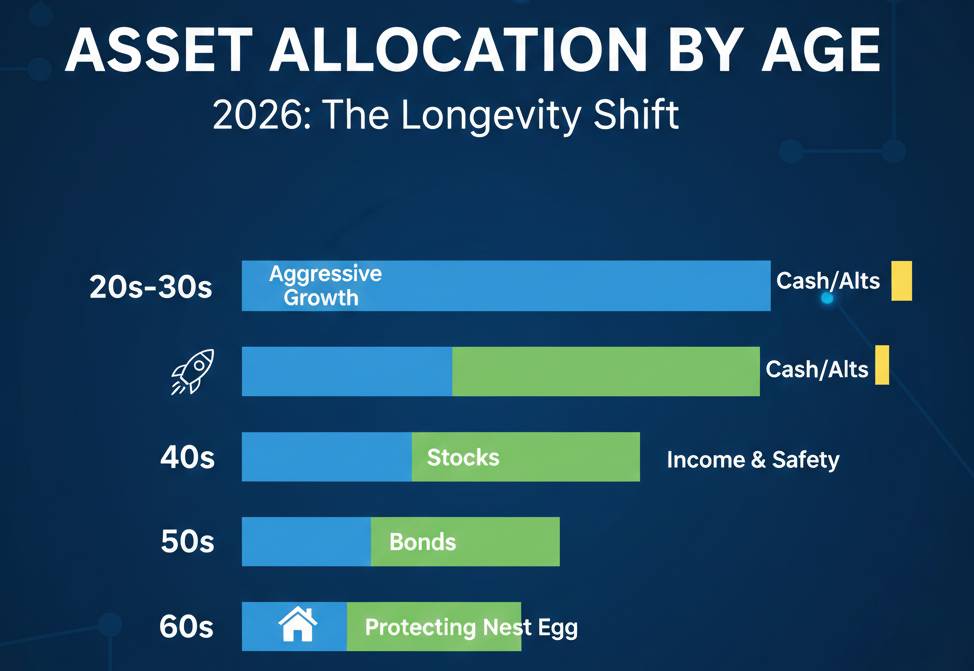

A Rough Cheat Sheet for Different Life Stages: Asset allocation by age

Since we’re talking about age, let’s look at a table that actually makes sense for the average person. But remember, please consult your financial advisor before taking any financial decision, especially if you have high liabilities.

| Life Stage | Age Range | Equity (Aggressive) | Debt (Stability) | Gold (Hedge) |

| Early Career | 22 – 30 | 70% – 80% | 15% – 20% | 5% |

| The Hustle Years | 31 – 45 | 60% – 70% | 20% – 30% | 5% – 10% |

| Pre-Retirement | 46 – 55 | 45% – 55% | 35% – 45% | 10% |

| The Golden Years | 56+ | 20% – 30% | 60% – 70% | 10% |

Breaking It Down: Why These Numbers?

The 20s: The “Take the Hit” Phase

When you’re in your 20s, time is your biggest asset. Even if the market crashes 30%, you have decades to recover. This is when you should be heavy on equity. Don’t obsess over “safety” in FDs yet. Your biggest risk at 25 isn’t a market crash; it’s not taking enough risk and letting inflation eat your small savings.

Keep a tiny bit in Gold maybe via Silver or Gold ETFs or SGBs just to get into the habit. Debt here should mostly be your emergency fund (6 months of expenses).

The 30s & 40s: The Balancing Act

This is the most stressful phase. You likely have a home loan, kids’ education coming up, and maybe some health scares in the family. You can’t afford to be 90% in equity anymore. If the market tanks right when your kid needs college fees,you’re stuck.

I usually suggest moving slightly more into Debt (PPF is great for the tax-free component) and keeping Gold at a steady 10%. Gold acts as a “peace of mind” asset here. When the world feels like it’s going to end, seeing your gold value go up helps you stay invested in your SIPs.

The 50s and Beyond: Protecting the Nest

At this stage, you aren’t trying to “beat the market” anymore. You’re trying to make sure you don’t run out of money. The shift towards Debt (Senior Citizen Savings Schemes, Debt Mutual Funds, etc.) is crucial. You want regular income and low volatility.

However, a big mistake people make is going 0% in Equity. With healthcare costs rising and people living until 85-90,you still need about 20-25% in Equity to make sure your corpus doesn’t lose its purchasing power over the next 30 years of retirement.

Why Gold is the “Underdog” You Actually Need

In India, we love physical gold. But as an investment, it’s often misunderstood. You shouldn’t buy gold thinking it will double in two years. Buy it because it has a low correlation with the stock market. Usually, when Nifty goes down, Gold goes up.

YOU CAN ALSO READ:

Credit score improvement plan : Useful Practical GuideThink of it like a spare tire. You don’t want to use it, and it sits in the trunk doing nothing most of the time. But when you have a flat tire (a market crash or high inflation), you’re glad you have it. I personally like Sovereign Gold Bonds (SGBs) because they give you 2.5% interest on top of the price appreciation. It’s a win-win.

How To Actually Set Up Your Asset Allocation

If you’re looking at your bank account right now and feeling overwhelmed, take a breath. You don’t have to fix everything today. Here’s a simple step-by-step way to get your house in order:

1. Calculate your Current “Real” Allocation Forget what you want to do. Look at what you have. Add up your EPF,PPF, FDs (Debt), your Mutual Funds and Stocks (Equity), and any gold ornaments or bonds you own. You might be surprised to find you are “Debt-heavy” because of your EPF, or “Gold-heavy” because of family inheritance.

2. Define your “Bucket” Needs Before moving money, ask: “When do I need this?”

- Money needed in < 3 years? Keep it in Debt (Liquid funds/FDs).

- Money needed in 3-7 years? 50-50 Equity and Debt.

- Money needed in 10+ years? Go 70% Equity.

3. The Rebalancing Act (Crucial!) This is where most people fail. Let’s say you decided on a 60:40 Equity to Debt ratio.After a massive bull run, your equity grows so much that your ratio is now 75:25. You feel like a genius, so you want to put more into equity.

Don’t. This is when you sell some equity and move it to debt to get back to 60:40. You are essentially “selling high” and “buying low.” It’s a mechanical way to be disciplined without letting emotions get in the way.

4. Automate the Boring Parts Set up SIPs for your Equity and a recurring deposit or VPF (Voluntary Provident Fund) for your Debt. If you have to think about it every month, you won’t do it.

Common Myths That Mess People Up

- “I’m too young to care about Debt.” No, you aren’t. Debt is for liquidity. If you lose your job, you can’t wait for the stock market to recover to pay your rent. Always have a debt buffer.

- “Real Estate is my asset allocation.” Real estate is great, but it’s “lumpy.” You can’t sell one balcony of your house to pay for a medical emergency. Treat your primary home as a lifestyle choice, not a part of this liquid asset allocation.

- “Gold is a bad investment because it doesn’t give dividends.” True, but it protects you against currency devaluation. If the Rupee falls against the Dollar, Gold usually gets a boost. It’s your global currency hedge.

A Note on the “Hinglish” Side of Investing

Dost, investing is 20% logic and 80% behavior. The best asset allocation on paper is useless if you sell everything the moment you see “Red” on your screen. Sukoon (peace) is the biggest return on investment. If a 70% equity allocation is making you lose sleep, it’s the wrong allocation for you, regardless of what your age is.

Lower the equity, increase the debt, and accept slightly lower returns for better sleep. It’s a trade-off worth making.

Final Thoughts

Asset allocation isn’t a “set it and forget it” thing. It’s more like a garden. You plant the seeds based on the season (your age), but you have to prune and weed it occasionally (rebalancing).

Whether you’re 25 and full of fire or 55 and looking for a quiet life, your money should reflect your reality, not some generic formula from a textbook. Start where you are, simplify your holdings, and remember that the goal isn’t to be the richest person in the cemetery it’s to have enough to live your life without constant money-stress.

YOU CAN ALSO READ:

Personal loan rejection reasons banks never explainImportant: The content shared here is just for pure educational purpose. Please don’t take it as financial advise and consult your financial advisor before taking any financial decision as they can help tailor a strategy that perfectly fits your individual profile and goals.

Explore more categories:

https://bylogic.xyz/category/investing-and-wealth-building/

https://bylogic.xyz/category/loans-and-credit/